2010 saw some significant changes in the way we consume digital content. Social media, video content and mobile are all changing the way marketers engage with consumers.

Leader in digital market measurement, comScore has released its latest report – 2010 Europe Digital Year in Review, which offers an overview of the digital landscape in Europe, examining trends in internet usage, social networking, online video, mobile and search.

Here are some key points from the report;

- Europeans spend the equivalent of one day a month online (24:20 hours)

- The Netherlands and UK Lead in Engagement, with the Netherlands (31:39 hours) and United Kingdom (30:38 hours) far exceeding the average

- More than half of Europe’s digital users are over the age of 35

- Of the more than 360 million online consumers in Europe, females represent a slightly larger percentage (48 percent) as compared to the worldwide average (46 percent)

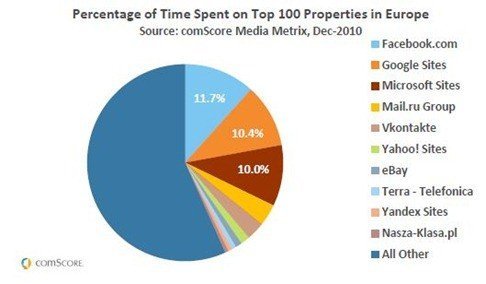

Europeans Spend More Time on Facebook than Any Other Site

Social Activities on the Rise

With many social networking sites in the top ranking for Europe, it’s no surprise that sharing constitutes the most popular behaviour on the web. Consumers are enjoying passing along photos, experiences and updates in order to stay connected. Instant messaging however has fallen out of favour with a decline of 8.3 percentage points versus a year ago. Auction sites are also proving less popular, with eBay for example losing 3.6 percentage points in 2010.

Instant Messaging Experiences Rapid Declines

Instant Messengers were once one of the most popular pastimes online but times have changed with consumers spending 39 percent less time using IM. In their place, Social Networking sites have eclipsed most other activities and are a magnet for consumers to while away their day with 34 percent more time spent social networking versus last year. Contrary to the US market, web-based email has remained a small but stable activity throughout 2010.

Email still popular among the older generation

While the younger generation (15-34 year olds) are increasingly shifting their online activity to social networking, the older population, above the age of 35, are experimenting with social networking but also embracing the comfort of traditional email.

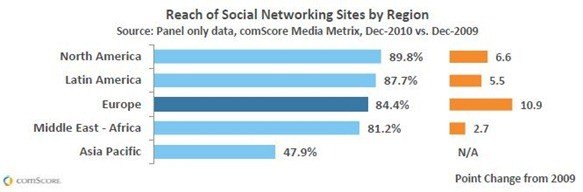

Social networking growth in Europe

- Europe shows the highest growth in social networking reach across regions

- By the end of the 2010, social networking monthly penetration in Europe reached 84.4 percent of all European internet users, representing a 10.9 percentage point gain – the highest of any global region

- Social networking accounted for 22.8 percent of all page views in Europe in 2010

- Approximately four out of every ten internet sessions included a visit to a social networking site

Social Networking Grows Across All Markets in Europe

The overall growth in the reach of social networking sites in Europe reflects growth across all markets. The Russian Federation showed the greatest growth with a 21.5 percentage point increase, followed by Germany (up 16.6 points). Austria, despite having the lowest social networking penetration overall, also experienced significant growth with a 16.3 percentage point increase.

Demographic Profile of Social Networking Users in Europe

- Women are leading in terms of engagement. In December 2010, women spent 24.3 percent of their online time on social networking sites, up 5.6 percentage points from a year earlier

- Men spent only 16.8 percent of their time on these sites, showing only a 3.1 percentage-point increase from 2009

These figures are well above the worldwide average, which shows women across the globe spending 18.3 percent of their online time on social networking sites. Compared to Europe, women worldwide spent less than a fifth of their time online on social.

The profile of social networking users in Europe also reveals an audience that generally skews younger;

- 15-24 year olds represent 25.3 percent of users

- 25-34 year olds represent 24.3 percent of users

While the breakdown of European visitors to Facebook and Twitter mirrors that of social networking site users in general, LinkedIn has an older age profile – only 10.4 percent of its visitors are under 25 years old, while half of the site’s audience is between the ages of 35-54. This older age profile is understandable given the site’s orientation toward professional networking.

Facebook and Social Networking Penetration by Market

By the end of 2010, Facebook was the leading social networking site in 15 of the 18 European markets included in this report.

- Only the Netherlands, Poland, and Russia have other social networks with audiences larger than Facebook

- Facebook currently has 48 percent of the monthly penetration in the Netherlands, ranking second to Hyves

- Facebook also ranks second in Poland with 55.5 percent penetration behind Nasza-klasa.pl

- Facebook has its lowest penetration in Russia, at 18.8 percent, currently lagging behind leaders Vkontakte, Odnoklassniki, and Mail.ru – My World.

Turkey had the highest Facebook penetration in Europe at 90.4 percent, followed by the UK at 81.7 percent. Nordic countries ranked in four of the next five spots, led by Finland (81.2 percent), Norway (79.7 percent) and Sweden (78.5 percent). Italy ranked sixth at 78.1 percent, while the fourth Nordic country Denmark followed at 77.5 percent

Markets Showing Greatest Facebook Growth

Although Facebook is not currently the leading social network in the Netherlands, it experienced significant growth in 2010 in that country and in several other European markets. In addition to the Netherlands, Facebook achieved its most significant gains in;

- Portugal (up 48.2 percentage points)

- Germany (up 35.7 points)

- Austria (up 27.2 points)

- Spain (up 18.5 points)

In April 2010, Facebook eclipsed the leading social networks in Portugal (Hi5) and Germany (StudiVZ/VZ-Netzwerke) to assume the #1 position among social networking sites in both those markets. The previous year, Facebook grabbed the #1 position in Spain (from Tuenti.com) and in Austria (from Netlog.com).

Advertising on Social Networking Sites Grows

As social networking becomes a more integral part of the online user experience, the presence of display advertising on social networking sites continues to grow.

- In the UK and France, total display ad impressions on social networking sites grew by 47 and 64 percent, respectively

- In Germany that number more than doubled

The increasing prevalence of social networking as a component of the display advertising landscape is an indication that advertisers cannot afford to overlook this channel given its potential to reach a large number of consumers with high engagement. Though advertisers have sometimes resisted advertising on social networks due to low click-rates, it is important to recognise that display ads have brand-building impact independent of driving clicks.

Online advertising in Europe

Display Advertising Reaches Over 97% of Users in UK, France, and Germany

In December 2010, internet users in the UK, France, and Germany received a total of 211.7 billion display advertisements

- UK market receiving the most ads at 71.4 billion

In all three countries, display ads reached over 97 percent of internet users.

Social Networking Drives Advertising Market

An analysis of the top categories serving display ads in December 2010 for the UK, France, and Germany showed Social Networking to be a key driver of display ad growth.

- Social Networking publishers accounted for the largest share of display ads in the UK, where they served a total of 41.3 percent of all display ad impressions during the month

- Services, which include Photos, Email, Instant Messengers, and Coupon sites, also served a significant portion of display ads across the three markets

The rise of coupon sites in Europe

Use of Coupon Sites Grows in Europe

The past year has seen online coupon sites emerge as an important channel in driving consumer behaviour in Europe, generating a 5.7 point increase in penetration. This growth is the highest seen in any region in 2010, bringing the reach of coupon sites in Europe to 9.6 percent of all internet users.

Groupon Contributes to Significant Growth for Coupon Sites in Europe

- The total number of people using coupon sites in Europe in a month grew 162 percent to 34.9 million visitors in December 2010 when compared to the prior year

- The sizeable growth can largely be attributed to the emergence of Groupon

- Groupon, buoyed by its acquisition of its leading competitor in Europe, was able to establish a presence in more than one hundred European cities in the past year and now reaches more than 12 million visitors a month, approximately one-third of the total coupon market

Use of Coupon Sites by Market

An analysis of individual European countries shows significant variation in the penetration of coupon sites.

- France continues to lead in having the highest monthly reach (20.6 percent of all French Internet users), followed by the UK (17 percent), and Italy (15.2 percent)

- Italy and Turkey experienced the most growth, with a 15.0 and 13.6 percentage point increase, respectively

Following tough economic conditions across Europe over the past number of years, it’s not a surprise to see the rise of money-saving couponing activity. The viral nature of major players, such as Groupon that encourage sharing of offers via Facebook and Twitter, will contribute to their continued growth and act as a bellwether to other online brands about the importance of making content and offers sharable.

Video growth in Europe

TV Sites Set for Continued Expansion in Europe

2010 was a strong year for TV web sites in Europe, with TV site penetration in the region increasing by 7.5 percentage points to 47.4 percent of all European internet users in December 2010 – second only to North America.

- Europe leads in engagement with TV sites

- The average European visitor spends 28 minutes visiting sites in this category each month

- German media giant ProSieben currently leads the European TV market with 32.5 million unique visitors in December – nearly twice the audience of the second-ranking French property Groupe TF1 at 16.5 million

- The German broadcaster ARD, the Italian Gruppo Mediaset, and the UK market leader BBC round off the list of top five TV properties for the region

- In December 2010, TV sites in Germany reached 16.3 million viewers, up 14 percent. France followed with the highest rate of change at 22 percent, with 15.0 million viewers

- The UK also showed strong growth at 19 percent, with 11.0 million viewers

Viewers in Germany, the UK, and Spain Spend the Most Time Watching Online Videos

While all countries in the EU5 (France, Germany, Italy, Spain, UK) show similar rates of penetration for the video market on the web, averaging 83.7 percent, the levels of engagement of users in these markets differ.

- In December 2010, viewers from Germany, the UK, and Spain spent more time watching online videos than those in the US, averaging 18.0, 17.0, and 16.2 hours respectively

- Viewers in France watched 12.2 hours of video and viewers in Italy watched the least with only 10.4 hours

- On average, the time EU5 video viewers spent watching online videos in December 2010 (14.8 hours) was just an hour short of how many hours the average viewer in the US spent watching videos in a month (15.8 hours)

Shift towards Longer Content is Shaping the Future of Online Video

Perhaps the most significant trend in 2010 for the European online video market was an increase in the average length of videos viewed, indicating a shifting preference to consuming fewer, longer videos.

- 2010 was the first year in which the number of online videos viewed decreased in the UK (down 6 percent), France (down 14 percent) and Germany (down 13 percent)

- However, the average length of videos viewed in UK, France and Germany increased by 13 percent to 5.6 minutes

- The changing demand has been both witnessed and driven by evolving strategies of top publishers, resulting in a growing supply of monetisable content

- The average length of videos viewed on YouTube – which accounts for 42.0 percent of videos viewed in the EU5 in December 2010 – increased by 9.5 percent in UK, France and Germany over the course of 2010

Online Video Viewing Dominated by Young Males

An analysis of the demographic composition of online video viewers shows younger males comprise the largest share of the audience.

- Within the EU5, under-35 year olds accounted for over half of time spent watching online video in December 2010

- Two-thirds of time spent watching online video is accounted for by males

- Viewing within the Entertainment category has a large impact on the skews. As an example, 16.3 percent of videos watched from Entertainment sites in the EU5 are watched by males age 15-24, with the highest ratio found in the UK (18.5 percent)

European mobile usage

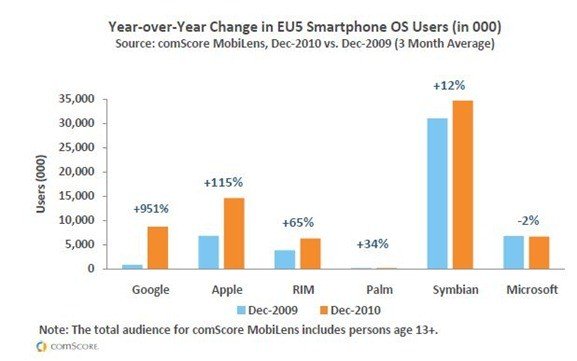

Smartphone Penetration in EU5 Continues to Increase

Smartphones continue to become an increasingly important segment of the European mobile phone landscape in 2010.

Smartphone penetration in the EU5 (United Kingdom, France, Germany, Spain, and Italy) increased by 9.5 percentage points to 31.1 percent, placing it higher than the US.

Analysis of the growth in smartphone reach in the EU5 reveals a dramatic increase in the adoption of Google and Apple smartphone operating systems.

- Google Android, which experienced a 951-percent gain in the use of its OS, now boasts an audience of 8.7 million subscribers in these five European markets

- Apple experienced a 115-percent increase to 14.5 million subscribers

- Symbian continues to lead the smartphone OS market

Market Enablers Help Grow Mobile Media Use

The overall growth in the use of mobile media can be attributed to the continued increase in penetration of several key market enablers:

- 3G device ownership – grew 5.4 percentage points to 47.1 percent penetration

- unlimited data plan subscription – plan subscriptions grew 2.5 percentage points to 7.5 percent

- Smartphone ownership – increased 9.5 percentage points in Europe during 2010 to 31.1 percent

European search market 2010

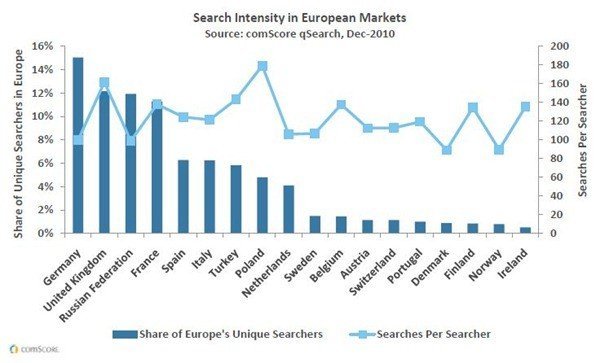

European Search Intensity Varies by Market

An analysis of individual search markets in Europe reveals differing levels of search intensity in these markets.

- Searchers in Poland exhibit the heaviest search intensity, with the highest number of searches per searcher across all markets

- Germany and Russia, which have significant shares of European searchers, show lower search intensity than in most markets, indexing below the European regional average

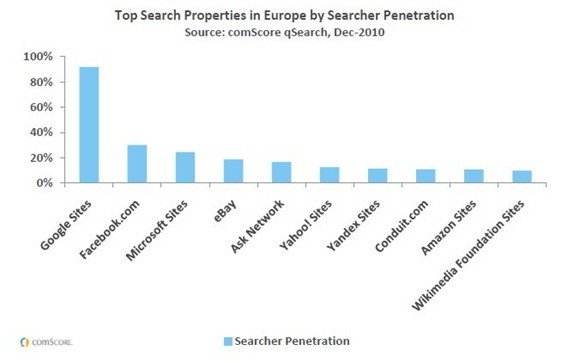

Google Continues to Lead Search in Europe

Google Sites continued to lead the search market in Europe, reaching 9 out of 10 Europeans in December 2010.

Facebook ranked second reaching 30.2 percent of the market and was the only social network in the list of top ten search properties.

2010 was undoubtedly a very exciting year for digital. We look forward to seeing what 2011 brings to the digital marketplace.

To download the full report, visit www.comscore.com.