Each year Hootsuite and We Are Social join forces to publish the Global State of Digital report, an overview of all things digital, including social media, search, ecommerce, advertising, and more. The report includes over 300 stats from over 230 countries worldwide to help digital marketers build their strategies for the year ahead.

If you want to read all 300 pages be sure to check out the full Global State of Digital 2022 report, but here we will take a look at some of the key stats and takeaways from the report. Unsurprisingly, these key findings are mostly tailored to the world of social media.

1. Social media use continues to grow

Social media platforms continue to go from strength to strength with more and more users creating new accounts year after year. This growth was evident through 2021 with near half a billion users creating a new social media account across the world. This accounts for a 10% rise in social media users compared to 2020 and takes the total number of social media users up to 4.62 billion (58% of the population).

Not only are more people using social media platforms, but they are also engaging with them more. The average time spent on social media has increased by 2 minutes a day to 2 hours and 27 minutes in 2021, compared to 2 hours and 25 minutes in 2020. Additionally, this time is spread over a variety of platforms with the average user engaging with over 7 different platforms each month.

2. The most popular social media platforms

Unsurprisingly, Facebook continues to dominate the world of social media by being the most popular platform by a fair distance. Its closest competitor is YouTube which is approximately 350 million active users behind, so it’s going to take some catching. WhatsApp, Instagram, and WeChat make up the rest of the top five, with TikTok just missing out in sixth place.

While the most used platforms may not throw up too many surprises, it is interesting to take a look at users’ favourite platforms. Facebook no longer reigns supreme here and has to settle for third place, behind WhatsApp and Instagram. However, I don’t think Facebook Inc., now Meta, will complain as they own the top three favourite social media platforms.

3. Changes in social media advertising

Social media advertising has continued to grow as total social media use has increased over the past year. That makes sense, more people are using the platforms, so surely it makes sense for marketers to dedicate more ad spend to these platforms, despite many brands tightening their budgets.

In 2021 social media advertising accounted for 33% of the world’s total digital advertising spend accounting for $154 billion worldwide. Not only is that a staggering amount, but it is also a 17% increase compared to 2020. This highlights how brands are seeing social media as a more effective way to reach their audience and potential customers.

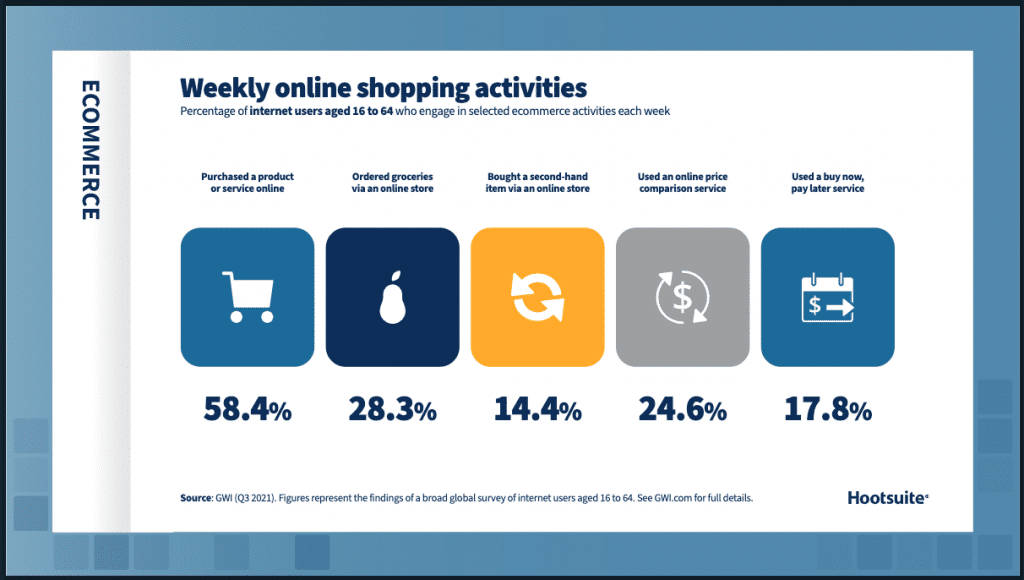

4. How do we shop online?

Here we move away from social media specifically, to take a look at how users engage with ecommerce activities on a weekly basis. Once again, this has seen a rise since 2020 with $3.85 trillion being spent on online consumer goods, an 18% increase. This is likely a result of the pandemic which has moved more businesses and users online, this is reflected by the fact that nearly 60% of internet users bought something online each week.

Brands can use this to boost their social strategy by ensuring they have a strong social store across multiple channels to ensure they are reaching a wide audience. Social media platforms are constantly improving their in-app shopping functionalities and by utilising them to the fullest brands can create a seamless experience for their customers.

5. Top channels for online brand search

Search continues to be the most popular channel for internet users to find information when researching brands, however, social networks are close on its tail. While it’s no surprise that search engines are at the top of the list, the findings become more interesting when looking at how different age groups research online. These findings look specifically at the difference in how social media and search engines are used for different age groups.

It’s interesting to see that the younger users (16-24 years old), actually use social media networks more than search engines to research brands. Additionally, for the next age band (25-34 years old), there is only a 1% difference. With that in mind, could we see the next wave of interest users moving away from the traditional search engines and utilising social platforms more and more for online shopping?

This only provides a brief overview of the full report. For more information be sure to check out the full document from Hootsuite and We Are Social for an overview of all things digital.